Did Vinted send you an email saying “Please confirm your status”? Are you exceeding €1,500 in annual sales and wondering if you’re compliant? This article sorts through rumors and actual thresholds in 2026, with a numerical simulation to help you decide.

⚠️ This article provides general information. For personal situations, consult an accountant or tax office.

The 2026 Context: DAC7 and the End of the Blind Spot

The European directive DAC7 (Directive on Administrative Cooperation), fully effective since January 2024 and strengthened in 2025, requires platforms like Vinted to automatically transmit to tax authorities:

- The seller’s identity

- Their IBAN

- The total annual transactions and number of sales

You can no longer “fly under the radar.” If you exceed the thresholds, the tax office will know.

The 3 Thresholds to Know

| Threshold | Trigger | Consequence |

|---|---|---|

| 20 sales/year OR €2,000/year | DAC7 | Vinted sends your data to the tax office |

| €305/year | Income tax | Mandatory declaration (box 1AJ or similar) |

| €77,700/year (BNC) or €188,700/year (BIC) | Micro-enterprise | Upper threshold, beyond = actual regime |

Note: DAC7 threshold ≠ tax threshold. The DAC7 threshold is the trigger for transmission, not the point at which you must start paying.

Selling Your Own Wardrobe: What Are the Rules?

If you are selling only your personal items (wardrobe clear-out), the tax regime depends on the nature of the item:

| Type of item sold | Tax regime | Exemption ceiling |

|---|---|---|

| Clothing, furniture, household appliances (personal use) | Non-taxable | No ceiling — exempt |

| Precious metals, jewelry > €5,000 | Capital gain | Mandatory declaration |

| Artwork, antiques | Capital gain | Above €5,000 |

In short: selling your second-hand clothes is never taxable, regardless of the amount (except for selling a Hermès bag for €8,000 → capital gain).

However, if you exceed the DAC7 threshold (20 sales / €2,000), Vinted will transmit your data. If you declare nothing, the tax office may ask you to prove that these items are indeed from your personal wardrobe. Be prepared to provide receipts or photos for major items.

Buying to Resell: Change of Regime

If you buy items specifically to resell on Vinted (buy-resell, consignment sales, thrift stores, flea markets), you are considered a merchant from the first sale. There is no tolerance threshold.

You must:

- Register as a micro-entrepreneur (free, in 15 minutes at autoentrepreneur.urssaf.fr)

- Choose the tax regime:

- BIC (Industrial and Commercial Profits) — this is the option for reselling goods

- Micro regime: a flat-rate deduction of 71% on revenue

- Declare your sales quarterly to URSSAF

- Report your income in the annual declaration

See Vinted for Professionals for the platform side of the status.

Numerical Simulation: 3 Typical Profiles

Here are 3 simulations based on real cases observed by Vinkit.

Profile A: Occasional Wardrobe Clear-Out

- 18 sales in 2026, €850 in revenue

- Personal items only

- No purchases for resale

Status: no change, no declaration needed. Tax to pay: €0.

Profile B: Intensive Wardrobe Clear-Out

- 45 sales in 2026, €2,800 in revenue

- Personal items only (typical testimony from Sophie)

- Vinted transmits to DGFiP (DAC7 triggered)

Status: no income tax due (sale of personal items), BUT you must be ready to justify that everything comes from your own wardrobe. Keep before/after photos, original receipts if possible. Tax to pay: €0.

Profile C: Regular Buy-Resell

- 80 sales in 2026, €5,200 in revenue

- €1,200 in purchases (Emmaüs, flea markets, consignment sales)

- Gross profit: €4,000

Status: must be registered as a micro-enterprise (BIC). Tax calculation:

- Micro flat-rate deduction (71%): €5,200 × 0.71 = €3,692

- Taxable income: €5,200 − €3,692 = €1,508

- Tax (based on your TMI at 11%): €166

- URSSAF social contributions (12.3% of revenue in BIC): €5,200 × 0.123 = €640

Total to pay: ~€806 (compared to €0 if you didn’t declare, but with a risk of reassessment + penalties).

The “Liberatory Payment” Option

If your TMI (marginal tax rate) is ≥ 11%, you can opt for the liberatory payment of income tax:

- 1% of revenue in BIC (reselling goods)

- 1.7% in BNC (services)

For Profile C above, this would result in a flat tax of €52 instead of €166. A net advantage.

The option must be requested before September 30 for the following year.

Vinted Pro: The Platform Feature

Distinct from the tax status, Vinted Pro (the feature) is a paid mode at €19.99/month on the platform, which allows:

- To display “Pro” on your profile

- To access extended statistics

- To benefit from reduced buyer commission fees (3.5% vs 5.5%)

- To have priority support

You can be registered as a micro-enterprise without subscribing to Vinted Pro (and vice versa). The two are independent.

For the feature, see Vinted for Professionals.

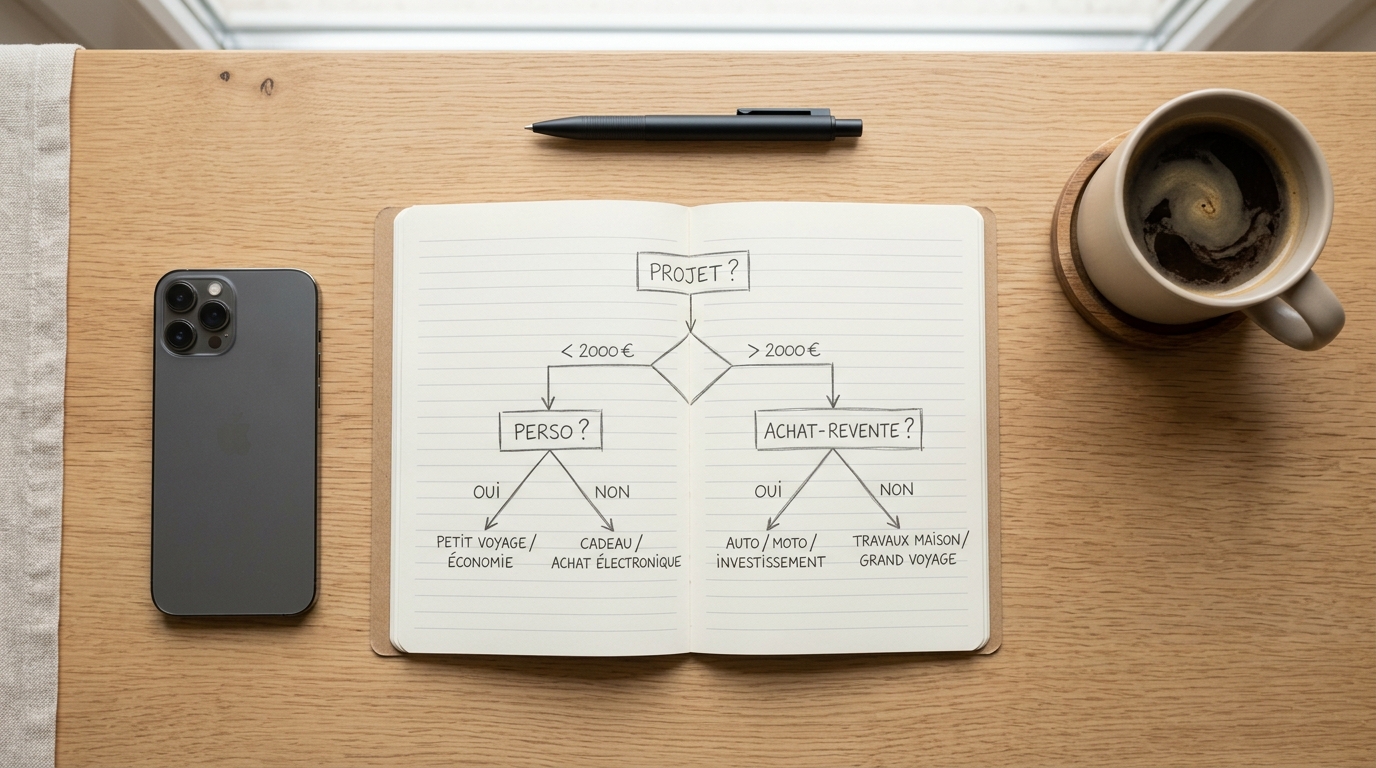

Quick Decision Tree

Your Vinted sales in 2026?

│

├── < €2,000 AND < 20 sales

│ └── Nothing to do, no DAC7 transmission

│

├── ≥ €2,000 OR ≥ 20 sales

│ │

│ ├── Only personal items?

│ │ └── No tax, but keep the proof

│ │

│ └── Buy-resell or regular activity?

│ │

│ ├── < €77,700 revenue

│ │ └── Micro-enterprise BIC (simple regime)

│ │

│ └── ≥ €77,700

│ └── Actual regime (accountant advised)

Pitfalls to Avoid

- “Vinted doesn’t send anything unless there are 30 sales”: false. The DAC7 threshold is 20 sales OR €2,000. Exceeding either of the two triggers transmission.

- “My friends don’t pay, so I don’t have to either”: just because others don’t declare doesn’t mean the risk is zero. The first reassessment letters from DGFiP to Vinted sellers were sent in April 2026.

- “The accountant is too expensive”: for revenue < €10,000, an online accountant (Indy, Shine, Qonto, Tiime) costs €15-25/month and handles 90% of the complexity.

- “I can declare in BNC to benefit from a better deduction”: no. Selling goods = mandatory BIC (71% deduction). BNC is for service provision.

FAQ

If I sell €2,500 in 2026 but it’s my own clothes, do I have to pay tax? No. The DAC7 threshold (€2,000) triggers a transmission, not a tax. Since these are personal items, you are not taxable. But keep proof in case the tax office asks.

What if I sell without declaring when I should? The risk is reassessment (up to 3 years back) + penalties of 40 to 80% + late interest. If the situation is recent, you can voluntarily regularize (reducing penalties to 0%).

Do I need to charge VAT? Below the micro threshold (€101,000 for BIC in 2026), no. Above that, yes (unless opting for VAT exemption).

Can I be both an employee and a Vinted micro-entrepreneur? Yes, it’s compatible and common. Just check your employment contract (possible exclusivity clause) and declare the dual status to URSSAF.

If I declare, does it change anything on the Vinted side? No. Your account functions the same. Vinted does not ask for your SIRET status.

In Summary

Three thresholds to remember for 2026:

- €2,000/year or 20 sales: Vinted transmits your info to the tax office (DAC7)

- €305/year: declaration threshold if commercial activity

- €77,700/year: maximum threshold for micro-enterprise BIC

Pure wardrobe clear-out = no tax even beyond the DAC7 threshold. Buy-resell = micro-enterprise from the first sale. If in doubt, an online accountant for €20/month clarifies everything in 30 minutes.

Next to read: Vinted Tax Obligations · Declaring Your Vinted Income to the Tax Office · I Sold €8,000 on Vinted in 6 Months